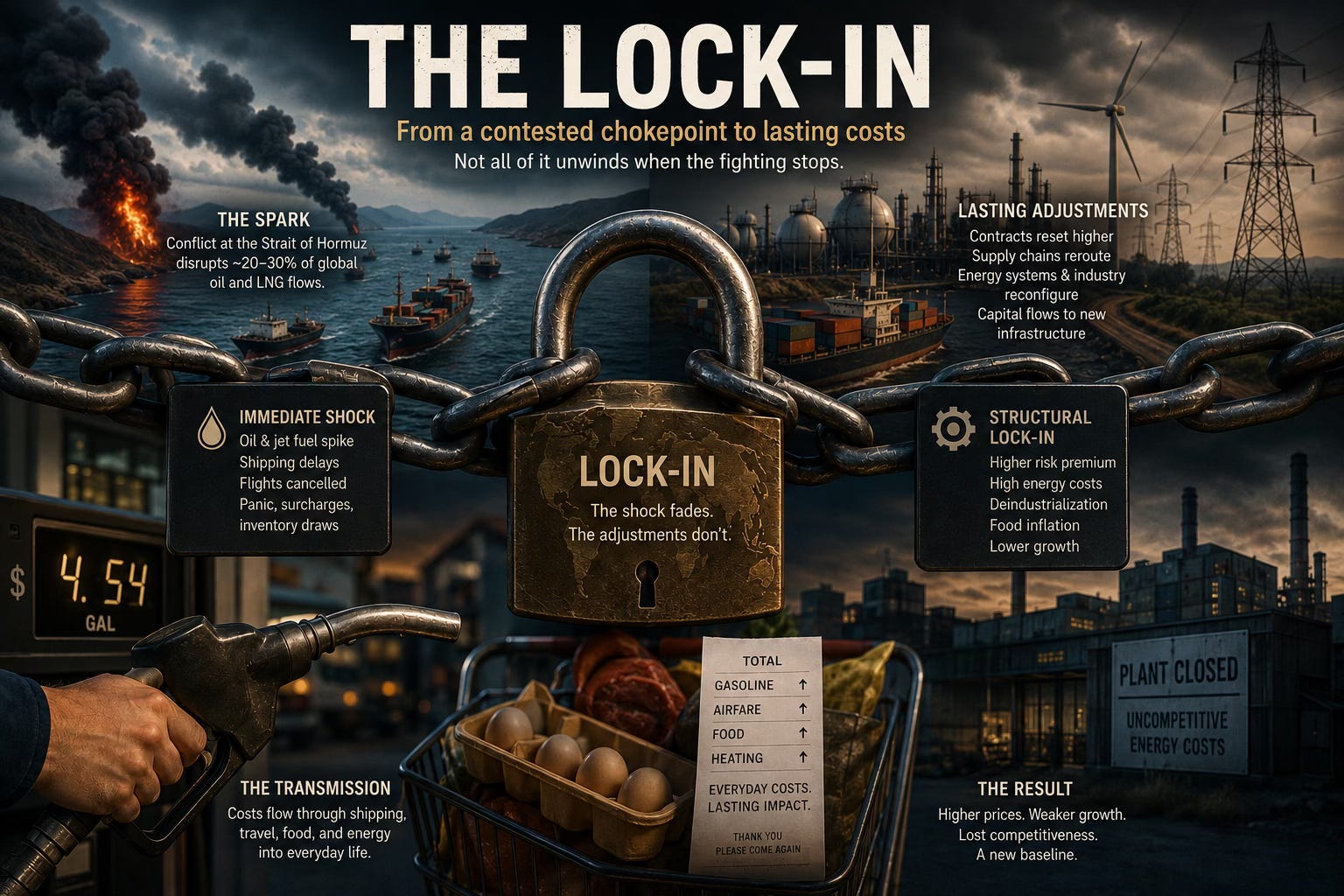

The Lock-In

Where the Iran War’s headline shock will unwind — and where it won’t.

This weekend, the US is waiting for Iran to reply to a memorandum that would end the war and open a 30-day negotiation window on nuclear issues and the future of the Strait of Hormuz. Russia and Ukraine agreed to a three-day truce to allow Vladimir Putin enough peace for a parade in Moscow, during which he said he thought the conflict was ‘coming to an end’. Donald Trump is packing for a state visit to see President Xi in China.

Meanwhile, some 1,600 ships remain stranded in the Gulf. France’s aircraft carrier Charles de Gaulle is crossing the Suez Canal towards the southern Red Sea, joining a multinational initiative to restore navigation and shipping through the Strait of Hormuz. The Royal Navy’s destroyer HMS Dragon is on its way to the Middle East to join forces. Iran has said passage through Hormuz may be possible under ‘new procedures’ that imply an Iranian toll-booth as part of any post-war settlement.

The point of writing at this moment, when markets are looking for relief and as headlines whiplash, is to distinguish between changes that might happen in the short term and conditions that have set in for the long term. The fact is that reopening a strait, or even patching up a conflict, does not unwind a lock-in.

We are witnessing in real time how a contested strait in the Persian Gulf becomes an inflation print in Iowa, how a drone strike near Hormuz becomes a higher grocery bill in Manchester three months later, or a disruption thousands of miles away becomes a factory slowdown in Germany, a cancelled flight at Heathrow, or a fertiliser surcharge in the American Midwest. The Iran war, like the Russia-Ukraine crisis, did not create these connections. They were there already. But it revealed them in plain sight and into the discussion. And what they represent is the defining feature of the modern energy system: that distance no longer protects anyone from dependency.

I appeared on Wednesday this week on Bloomberg Surveillance to discuss the energy and inflation implications of the conflict. Walking out of the studio in Manhattan, so far from the flashpoint, one thought kept returning: almost every major economic vulnerability in this episode traces back to the same underlying condition: lock-in. We were now talking not only about dependence on imported energy, but dependence embedded into infrastructure, supply chains, procurement systems, industrial policy, buildings, grids, financing assumptions, and political habits accumulated over decades. The world has not suddenly become fragile. It lost the ability to pretend that it isn’t and we are now talking about it.

This Substack is partly about what this severe Middle East disruption means next for households, markets, and industry. But it is also about something larger: the next phase of global competition, and the systems that the world can’t easily unwind.

The First Lock-In: At the Kitchen Table

It is easy to frame energy insecurity when you can relate geopolitics to a household’s budget.

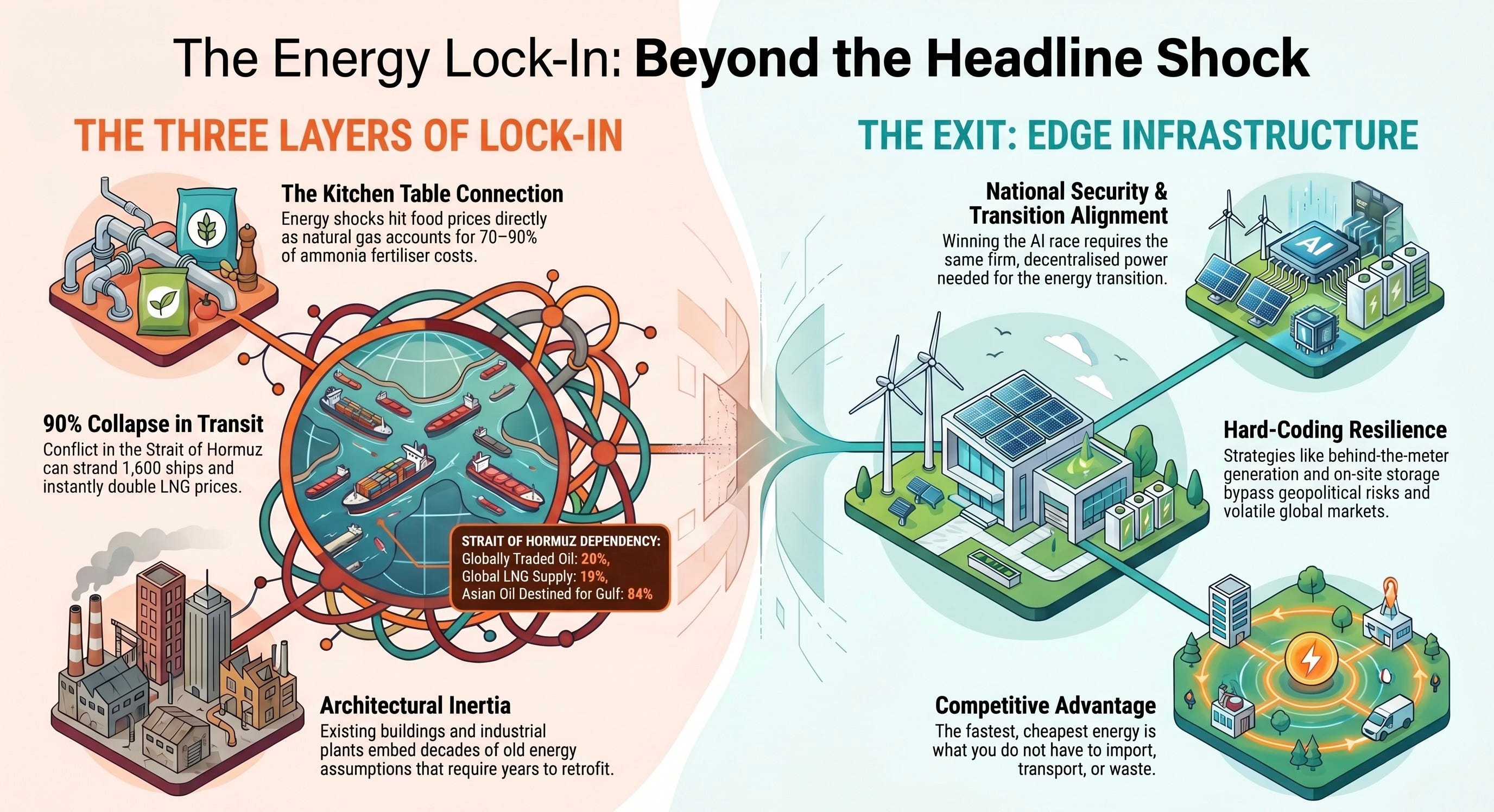

The Strait of Hormuz carries roughly one-fifth of all globally traded oil, around 19% of the world’s LNG supply, and approximately 13% of globally traded chemicals, including fertilisers. Since the conflict began, shipping traffic through the strait has fallen by more than 90%, with around 1,600 vessels currently stranded. Two US-escorted commercial ships have transited successfully under Project Freedom — now paused. The rest of the global fleet is waiting.

The first-order effects of this disruption are immediate and visible: higher petrol prices, more expensive jet fuel, freight disruption, tighter industrial energy markets, and sharply increased shipping insurance. These move markets within days. But it is the second-order effects that you can feel, and that endure longer.

Food inflation comes next. The mechanism is direct: natural gas accounts for between 70% and 90% of the variable cost of producing ammonia, the building block of all nitrogen fertilisers. Half of all food consumed globally depends on synthetic nitrogen fertilisers made through the Haber-Bosch process. When energy prices spike, fertiliser prices follow within weeks; harvest economics follow within months; and supermarket prices follow months after that. The World Bank is already projecting a 31% increase in global fertiliser prices for 2026, with urea — the world’s most widely used nitrogen fertiliser — having jumped roughly 46% in a single month earlier this year.

Then come industrial closures. Household energy bills rise. Manufacturing output weakens. Consumer confidence retreats. These effects take months to fully emerge, and longer still to fully abate.

The United States feels this primarily at the pump and in transportation costs. Europe feels it more broadly: chemicals, heating, fertiliser, steel, industrial production, food, electricity.

But the worst-affected economies are not in the West. In 2024, around 84% of crude oil passing through the Strait was destined for Asian markets. China, India, Japan, and South Korea together account for roughly three-quarters of Gulf oil exports and nearly 60% of its LNG. LNG spot prices in Asia more than doubled within days of the closure reaching $25 per million BTU, and have since risen by more than 140%. The countries bearing the sharpest immediate pain are not the G7 economies with deep reserves and policy tools, but Pakistan, Bangladesh, Vietnam, and the archipelago economies of South-East Asia — where fuel rationing, university closures, and restrictions on commercial activity are already in force, and where the IEA is projecting GDP growth cuts of up to 1.3 percentage points across developing Asia and the Pacific. Africa faces a parallel crisis through a different channel: higher fertiliser and fuel import costs are compounding food insecurity across sub-Saharan economies that were already operating with minimal fiscal headroom. Zimbabwe, Nigeria, and others have reported severe fuel shortages. The disruption to flight corridors between Africa, Asia, and Europe has added a further layer of economic isolation. For these countries, the Hormuz crisis is not a price signal, but a welfare shock.

Europe has already discovered that replacing Russian gas with LNG from elsewhere does not eliminate vulnerability. It merely changes its form. LNG now accounts for roughly half of Europe’s total gas supply, with the United States providing around 57% of those LNG imports — a dependency that has nearly quadrupled since 2021. The EU has spent approximately €380 billion on pipeline gas imports since 2022 alone, largely substituting one geopolitical exposure for another. The underlying architecture remains exposed to imported marginal molecules whose price is set by events far beyond domestic control. The root problem is not only the choice of supplier, but the dependence itself.

Dependence once looked rational. Cheap fossil energy appeared abundant. Supply chains appeared stable. Energy security appeared largely solved. That era is ending. And the most dangerous thing about lock-in is that it compounds silently for years before revealing itself all at once.

The Second Lock-In: What a Deal Does Not Unwind

A question haunting markets now is whether a peace deal would reverse the shock.

The answer, or hope, must be partially, yes. Oil markets would likely retrace much of any panic spike. Freight rates would ease. Aviation fuel premiums would normalise. Equity markets would rerate transport-sensitive sectors. But several things don’t fully unwind.

The first is the risk premium itself. Once a strategic chokepoint demonstrates vulnerability at this scale — a 90%-plus collapse in transit volumes, 1,600 ships stranded, the first sustained closure of Hormuz in the modern era — markets will find it hard to forget. Insurers, utilities, commodity traders, manufacturers, governments, and procurement officers all begin pricing disruption differently. The option value of instability becomes embedded into hedging costs, inventories, infrastructure planning, and investment decisions. That repricing tends to persist for years rather than months. Notably, Iran has already signalled that any post-war framework for the strait will reflect what it calls “a new balance of power” — language that suggests the old but fundamental assumption of unconditional freedom of navigation may be tested.

The second is food inflation. The fertiliser shock is already in the system. Urea prices are elevated and may not fall immediately or quickly if a memorandum is signed; planting decisions for the 2026–2027 season are already being made under current cost structures; and harvests will reflect those decisions regardless of what happens next. Energy shocks routinely outlive the headlines by twelve to eighteen months.

The third is infrastructure procurement. Hyperscalers, manufacturers, hospitals, infrastructure funds, and governments do not unlearn what shocks teach them. Behind-the-meter generation, redundancy, on-site storage, local resilience, and flexible energy systems are being hard-coded into procurement requirements and capital plans.

That structural shift matters much more than the short-term oil spike itself. This is why episodes like this are not merely trading events. They are investment moments. Oil prices may fall sharply, diplomacy may stabilise the Gulf, recession may suppress demand before structural shortages emerge. But lock-in means that even temporary shocks leave permanent fingerprints.

The Third Lock-In: Two Decades of Architecture

Most of the buildings that will exist in 2045 already exist today. Most industrial systems are long-lived. Most transmission infrastructure takes years — often decades — to plan, permit, and construct. The United Kingdom and much of Europe remain heavily exposed to gas pricing within electricity markets not because of any single policy failure, but because of decisions about generation mix, network architecture, and import dependency accumulated across administrations, technology cycles, and energy regimes.

Think of a steel plant built in the Ruhr in the 1990s, a hospital wing opened in Manchester in 2005, or a data centre commissioned in Dublin in 2019. Each was designed around the energy system that existed at the time — the grid connections available, the gas prices prevailing, the infrastructure assumptions of its era. Retrofitting any of them is not a procurement decision. It is a capital programme, measured in years and tens of millions. The building fabric, the plant rooms, the process design, the financial model: each embeds the energy assumptions of the moment it was built, and each compounds them forward across its operating life.

The United States differs for one critical reason. It is an energy superpower and net exporter. The same molecule traded globally carries an opposite trade balance — and a completely different political outcome.

That is the deeper lock-in: not merely geopolitical dependency, but physical dependency embedded into buildings, industry, transport and society itself. No memorandum of understanding, however carefully worded, can rapidly unwind that.

The Pacific Lock-In — Where Security and Transition Converge

The next major question is what Washington does strategically once Middle East tensions eventually ease. The centre of gravity shifts toward the Indo-Pacific: semiconductors, AI, advanced manufacturing, supply-chain resilience, critical minerals, computational infrastructure, and energy abundance.

But here is a point that much of the commentary misses: the information technology competition — between the United States, China, and the economies that will ultimately choose sides — is largely a competition over electricity. AI training and inference at frontier scale require not merely abundant power but reliable, cheap, firm power. Preferably at the point of use. Preferably insulated from geopolitical supply chains. Preferably immune to the disruptions that unfold when a tanker is struck in the Gulf of Oman.

That is a description of decentralised, efficient, resilient energy infrastructure. It is also, almost word for word, a description of what energy transition advocates have argued for on climate grounds for two decades. For the first time in the history of energy geopolitics, the requirements of national security and the imperatives of the energy transition may point in exactly the same direction and be talked about as such. The great powers cannot win the AI race without building the distributed, low-carbon, resilient infrastructure that the climate requires. This is not a coincidence. It is a structural alignment — and potentially the most powerful forcing function the transition has ever had.

The constraint is not the resource. Unlike oil, the underlying energy here is physics: photons hitting solar panels, wind moving turbines, heat differentials, electrochemistry. None of these exhaust. The constraint is the architecture. And architecture takes time.

Computational advantage compounds exponentially. The lag time between a policy decision to build resilient energy infrastructure and the day that infrastructure goes live has historically been measured in years, not months. The countries that close that gap fastest will not merely decarbonise. They will win.

The Exit

The consequential question is therefore not merely where the lock-in reveals itself. It is what the exit looks like – what we are going to do about it and who is going to do it first.

What would make a hospital, an industrial facility, a datacentre, a defence asset more resilient today? Not a new hospital. A behind-the-meter energy system, optimising for combined electrical and thermal efficiency. A building fabric retrofit. On-site battery storage. A heat network connection. A long-term energy contract that caps the price of power for a decade regardless of what happens in the Strait of Hormuz.

None of these require a geopolitical breakthrough. None require waiting for a new government. None, indeed, require importing a single additional molecule of gas or drop of oil. This is what I mean by EDGE infrastructure. It is not a technology category, but a strategic posture.

The economics stand on their own. Lead times for distributed energy and efficiency infrastructure are often dramatically shorter than those for grid-scale generation or major transmission. Customers are starting to be willing to pay for certainty, resilience, price stability and total cost of ownership and operations. That is especially true for hyperscalers, advanced manufacturers, hospitals, logistics infrastructure, and institutional real estate.

We are no longer having a climate argument. We are putting forward a competitiveness argument, a security argument, and an industrial strategy argument simultaneously. Every civilisation ultimately reorganises itself around the cheapest reliable source of energy available to it.

The fastest, cheapest, most resilient energy is ultimately the energy you do not have to import, transport, hedge, insure, burn or waste.

The Hardest Thing About Lock-In

The hardest thing to convey about lock-in is not its scale. It is its rhythm.

The danger is not the shock itself. The shock is visible, legible, priced. The danger is the period of normal that follows — the often protracted period when the lesson has been learned in public but not yet acted upon in private, when the urgency fades and the procurement decisions quietly revert to old habits, when another critical infrastructure or industrial asset gets built around imported energy assumptions and another data centre gets designed for fragile grid dependency.

We have been here before. The 1973 oil embargo generated a decade of intense Western focus on energy efficiency and diversification: insulation programmes, vehicle efficiency standards, nuclear build-out, demand management. Then, as oil prices fell through the 1980s, the urgency dissipated. The structural investments were never completed. The architecture reverted toward cheap dependency. And thirty years later, the same vulnerabilities reasserted themselves, sometimes wearing different geopolitical clothes, but expressing the same underlying condition.

The good news is that the technologies to exit these dependencies already exist. The economics work. Buyers are motivated. What has most often been missing is not innovation, not capital, nor even political will in the abstract. It is memory and desire for change.

The competition for resources has been the through-line of this Substack from the beginning: Ukraine, Greenland, Venezuela, Iran, the Indo-Pacific, AI infrastructure. Each episode is different on the surface, but the underlying logic and pattern is consistent throughout.

The lock-in that ultimately persists is not the one that couldn’t be solved. It is the one that was solved, forgotten, and then quietly inherited again.

My hosts at Bloomberg asked me whether anything will change this time. We have been given the analysis, the technology, and the economics.

History is not obliged to give us a third chance.

Jonathan Maxwell is the CEO of Sustainable Development Capital LLP and author of The Edge. He writes about energy, climate, finance, and geopolitics.

Views expressed are personal and do not constitute investment advice.

To learn more about energy efficiency, visit the website of SEIT plc, or SDCL Group.